The recent events of the previous quarter (1Q 2022) tested active managers. The Aapryl Quarterly Market Insight offers a lens on how active managers in general performed in various markets and sub-segments. Using Aapryl’s proprietary methodology, we measure manager skill by using the manager’s static clone (long term factor profile) as a measure of skill instead of the broad market benchmark. Manager skill is calculated by using the manager’s raw return less their static clone return.

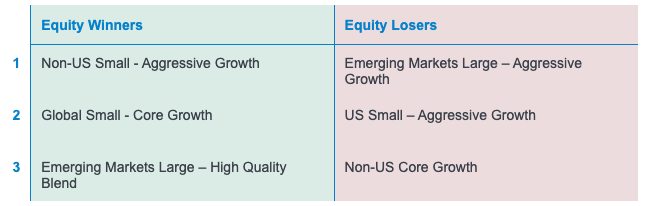

Below are the winners and losers of the prior quarter based on their respective peer group medians:

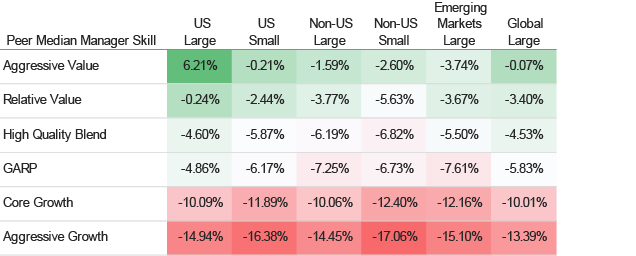

Aapryl Peer Group Manager Skill Performance Matrix

Quarter Ending 3/31/2022

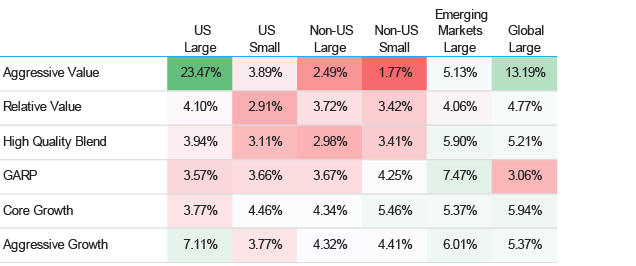

The performance spread of top performers vs bottom performers within their respective peer groups widen during the quarter from a high positive spread of 5.45% in Global Small GARP and a negative spread of 6.25% in Non-US Small Aggressive Value.

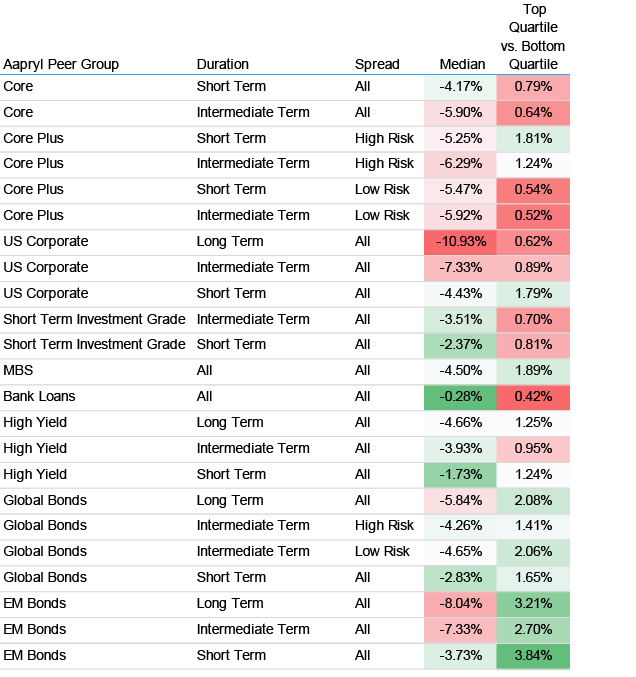

Top Quartile vs. Bottom Quartile Spread

Quarter Ending 3/31/2022

Active managers in Fixed Income were able to add value (manager skill) across the board with the best peer median performance in Emerging Market Debt and the least performer US Fixed Core with 0.35% peer median return for the quarter. Spreads range as high as 1.25% in Emerging Market Debt and as low as 0.65% for both US Fixed Core and US High Yield.